1. What is the Solid State Drives (SSD) Market Overview – Definition, scope, and significance?

The Solid State Drives (SSD) market comprises the design, manufacture, and distribution of flash‑based storage devices that replace traditional mechanical hard drives. SSDs are used in a wide range of applications, from consumer laptops to enterprise data centers, offering faster data access, lower power consumption, and greater durability. The market’s scope includes internal and external SSDs across multiple storage capacities, various NAND flash technologies (SLC, MLC, TLC), and end‑users such as industrial, automotive, enterprise, and client segments. Its significance lies in driving digital transformation, enabling high‑performance computing, and supporting emerging workloads like AI, edge computing, and 5G‑enabled devices.

2. What are the Solid State Drives (SSD) Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the rapid adoption of cloud services, increasing data‑intensive applications, and the need for energy‑efficient storage in data centers. The decline in NAND flash prices and the expansion of 3D‑stacked technology further accelerate demand. Restraints stem from supply‑chain constraints for semiconductor wafers and the higher upfront cost of SSDs compared with HDDs. Challenges involve maintaining cost‑performance balance as capacities increase and addressing data security concerns in high‑growth verticals like automotive. Opportunities arise from the growth of NVMe over PCIe, the rise of edge AI devices, and the shift toward all‑flash data‑center architectures, which open avenues for higher‑value, premium‑priced products.

3. What are the current Solid State Drives (SSD) Market Growth Trends?

Current trends feature a strong migration to NVMe‑based SSDs, driven by superior bandwidth and latency improvements over SATA interfaces. The adoption of PCIe 4.0 and early PCIe 5.0 standards is expanding performance ceilings, especially in enterprise and gaming markets. Another trend is the increasing use of QLC (Quad‑Level Cell) NAND to deliver larger capacities at lower cost, while SLC and MLC remain preferred for high‑end, mission‑critical workloads. OEM integration of SSDs into ultrathin laptops and tablets continues, and the automotive sector is moving toward solid‑state storage for infotainment and autonomous driving platforms.

4. How has COVID‑19 impacted the Solid State Drives (SSD) Market and what is the recovery trajectory?

The pandemic caused an initial slowdown in manufacturing due to lockdowns, but also triggered a surge in remote work, e‑learning, and home entertainment, which boosted demand for consumer SSDs. Data‑center expansions accelerated as enterprises embraced hybrid‑cloud models, reinforcing enterprise‑grade SSD sales. Supply‑chain disruptions gradually eased in 2022, and by 2023 the market entered a robust recovery phase, supported by strong component availability and renewed investment in digital infrastructure. The trajectory remains upward, with continued resilience expected as the world adapts to post‑pandemic digital norms.

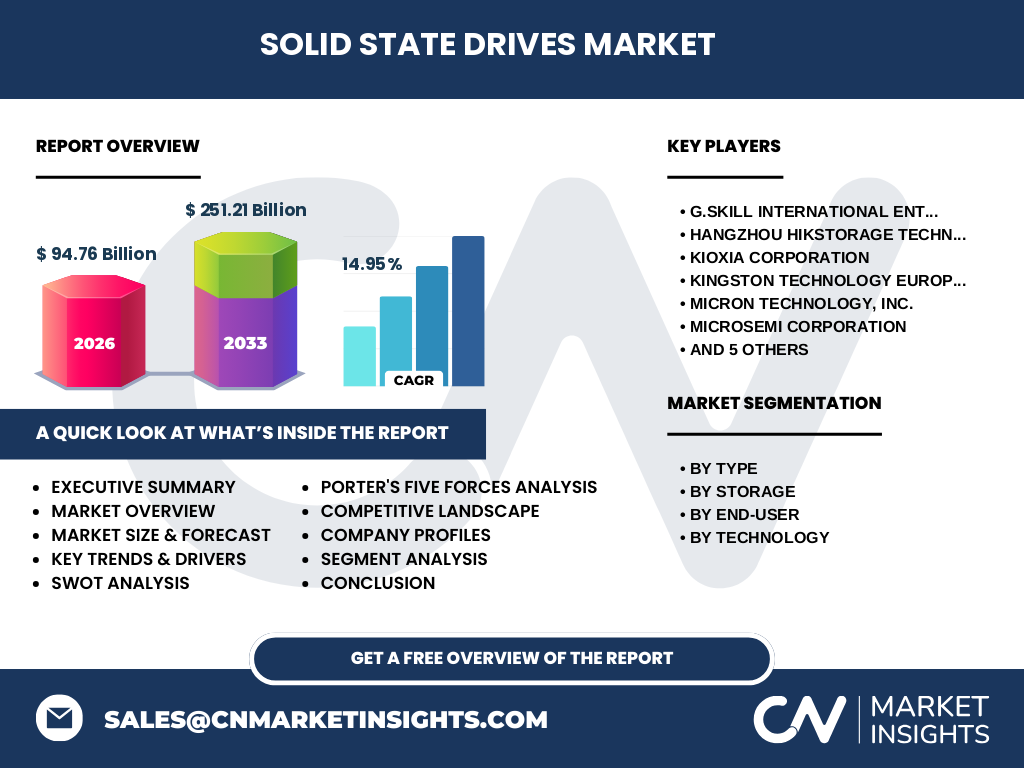

5. What does the Solid State Drives (SSD) Competitive Landscape look like – major competitors and market consolidation?

The SSD market is highly competitive, featuring a mix of long‑standing memory giants and specialist storage firms. Leading players include Samsung Group, SK Hynix Inc., KIOXIA Corporation, Micron Technology, Inc., and Western Digital Corporation, which dominate the NAND supply chain and high‑volume SSD production. Companies such as G.SKILL International Enterprise and Kingston Technology focus on performance‑oriented consumer segments, while Silicon Power and Seagate Technology expand niche offerings in external SSDs. Recent years have seen modest consolidation through strategic acquisitions and joint ventures aimed at securing NAND capacity and expanding firmware capabilities.

6. What are the key findings in the Executive Summary of the Solid State Drives (SSD) Market?

The SSD market is positioned for rapid expansion, with a 2026 valuation of USD 94.76 billion and a projected increase to USD 251.21 billion by 2033, reflecting a robust CAGR of 14.95 %. Growth is powered by enterprise data‑center migration to all‑flash arrays, rising consumer demand for high‑speed storage, and emerging applications in automotive and industrial IoT. The internal SSD segment holds the largest share, while external SSDs benefit from mobile and gaming use‑cases. NAND technology diversification (SLC, MLC, TLC) sustains product differentiation. Competitive dynamics are shaped by vertical integration of memory producers and aggressive innovation from component‑focused firms.

7. What is the Solid State Drives (SSD) Market Forecast for 2025‑2032?

Based on the stated CAGR of 14.95 %, the market is expected to maintain strong double‑digit growth through 2032. The forecast foresees continued expansion of enterprise‑grade NVMe SSDs, propelled by AI and high‑performance computing workloads. Consumer segments will benefit from the rollout of next‑generation gaming consoles and ultrabooks that prioritize low latency storage. By 2032, the market is anticipated to surpass the USD 250 billion mark, indicating a mature but still expanding ecosystem where premium, high‑capacity SSDs become the norm across most device categories.

8. How is the Solid State Drives (SSD) Market Size and Share broken down by segmentation?

Segmentation occurs across four dimensions. By type, the market splits into internal SSDs (dominant due to OEM integration) and external SSDs (growing in portable storage). By storage capacity, categories range from under 500 GB to above 2 TB, with the 1 TB‑2 TB band capturing the highest volume as it balances cost and performance for both consumer and enterprise users. By end‑user, the enterprise segment leads in revenue, followed by client (PC and laptop) markets; industrial and automotive segments are smaller but expanding rapidly. By technology, Single‑Level Cell (SLC) serves premium, low‑latency needs, Multi‑Level Cell (MLC) targets mid‑range performance, while Triple‑Level Cell (TLC) offers cost‑effective high‑capacity solutions.

9. What is the Global Solid State Drives (SSD) Market Size and Share by Region?

While exact regional dollar figures are not disclosed, the market exhibits strong presence across North America, Europe, Asia‑Pacific, and emerging economies in Latin America and the Middle East. Asia‑Pacific leads in manufacturing capacity, driven by Taiwan, South Korea, and China, which host many of the key semiconductor fabs. North America and Europe dominate enterprise SSD adoption due to high data‑center density and early technology uptake. Regional growth rates are aligned with local digital transformation initiatives and consumer electronics demand.

10. What does the Regional Analysis of the Solid State Drives (SSD) Market reveal?

In North America, enterprise migration to all‑flash arrays and high‑performance computing research fuel demand. Europe mirrors this trend, with added emphasis on sustainability, prompting a shift toward lower‑power SSD solutions. Asia‑Pacific combines strong manufacturing capability with burgeoning consumer markets, especially in China and India, where smartphone and laptop penetration drive internal SSD sales. Latin America shows gradual growth as data‑center investments increase, while the Middle East and Africa display niche expansion tied to oil‑and‑gas analytics and government digital programs.

11. Which companies lead the Solid State Drives (SSD) Market and what are their strategic approaches?

Samsung Group leverages its vertically integrated NAND production to deliver high‑performance PCIe 4.0 and 5.0 SSDs for data centers. SK Hynix focuses on scaling 3D NAND capacity and cost efficiency. KIOXIA (formerly Toshiba Memory) capitalizes on its expertise in automotive‑grade flash. Micron Technology invests heavily in QLC and emerging 3D‑XPoint technologies. Western Digital combines HDD heritage with flash solutions through its SanDisk brand. Kingston Technology and G.SKILL target gamer and enthusiast segments with overclocked, low‑latency modules. Seagate and Silicon Power expand external SSD portfolios, emphasizing rugged designs for mobile professionals.

12. How does Porter’s Five Forces analysis apply to the Solid State Drives (SSD) Market?

Threat of new entrants is moderate; high capital requirements for NAND fab construction limit newcomers, but fab‑less design firms can enter with innovative firmware. Bargaining power of suppliers is relatively high, as a few semiconductor manufacturers control NAND supply. Bargaining power of buyers is moderate; large OEMs negotiate volume discounts, yet fragmented consumer markets retain price sensitivity. Threat of substitutes is low; HDDs remain slower and less power‑efficient, making SSDs the preferred upgrade path. Competitive rivalry is intense, driven by rapid technology cycles, frequent product launches, and pricing pressure across all segments.

13. What are the SWOT insights for the Solid State Drives (SSD) Market?

Strengths: Superior performance, decreasing cost per GB, and broad applicability across industries. Weaknesses: Higher upfront price relative to HDDs and reliance on complex semiconductor supply chains. Opportunities: Expansion into edge AI, 5G infrastructure, and automotive infotainment, as well as growth of NVMe over Fabrics. Threats: Potential supply disruptions, emerging competing memory technologies (e.g., MRAM), and regulatory scrutiny over data security.

14. How is the Solid State Drives (SSD) Value Chain structured?

The SSD value chain begins with raw silicon wafer procurement, followed by NAND flash cell fabrication (memory fabs). These wafers are then assembled into SSD modules by integrated device manufacturers, which add controller ASICs, firmware, and packaging. Distribution occurs through OEM partnerships, channel distributors, and direct retail for consumer products. After‑sales services, firmware updates, and data‑recovery solutions complete the chain, adding value throughout the product lifecycle.

15. What key investment insights can be drawn for the Solid State Drives (SSD) Market?

Investors should prioritize companies with owned NAND capacity and strong NVMe roadmaps, as these are positioned to capture premium data‑center spend. Partnerships that secure long‑term supply of advanced 3D NAND (e.g., 176‑layer and beyond) are a critical moat. Venture funding in firmware‑optimization startups and edge‑AI storage solutions presents high‑growth ancillary opportunities. Geographic diversification, especially exposure to Asia‑Pacific manufacturing hubs, mitigates regional supply risks.

16. What conclusions can be drawn about the Solid State Drives (SSD) Market?

The SSD market is on a decisive upward trajectory, driven by relentless demand for speed, energy efficiency, and reliability across both consumer and enterprise domains. With a projected valuation of over USD 250 billion by 2033 and a near‑15 % CAGR, the sector offers substantial growth potential. Technological innovation—particularly NVMe, PCIe 5.0, and advanced NAND architectures—will continue to differentiate players. While supply‑chain and cost considerations persist, the overall outlook remains strongly positive.

17. How was the research for this market report conducted?

The study combined primary interviews with industry executives, supplier surveys, and secondary data analysis from company filings, market databases, and reputable research firms. Trend extrapolation employed the provided CAGR of 14.95 % to forecast future market size. Segmentation analysis leveraged the defined categories (type, storage, end‑user, technology) to structure insights. Competitive mapping integrated public announcements, product roadmaps, and merger activity.

18. What is the scope of this research and its limitations?

The scope covers global SSD market dynamics from 2026 to 2033, focusing on internal and external SSDs across defined capacity, end‑user, and technology segments. It includes major geographic regions and the leading 11 companies listed. Limitations arise from the reliance on publicly available financial figures and the exclusion of proprietary market‑share percentages, which prevents detailed quantitative breakdowns beyond the aggregate size and CAGR provided.

19. Which key companies have made recent developments in the Solid State Drives (SSD) Market?

Samsung Group announced a new PCIe 5.0 SSD line targeting hyperscale data centers, emphasizing sub‑microsecond latency. SK Hynix launched a 176‑layer 3D NAND platform, promising higher density at lower cost. Micron Technology introduced a QLC‑based consumer SSD with integrated heat‑dissipation technology. Kingston Technology released a high‑performance gaming SSD featuring RGB lighting and proprietary firmware tuning. Western Digital’s SanDisk brand unveiled an external SSD with IP‑68 waterproof rating for rugged field use. Seagate announced a partnership with a leading automotive OEM to supply SSDs for next‑generation infotainment systems.